Portraying the Israeli Software Development Life Cycle (SDLC) industry and sharing insights from SDLC-focused startups and their customers

At Grove Ventures, software infrastructure is one of the major pillars of our investment strategy. For this reason, every so often, we gather some of Israel’s top software infrastructure leaders to discuss up-and-coming software development life cycle (SDLC) trends. Last year, something unusual occurred: we all agreed that what was actually happening in the market was different than what many in the industry were preaching about. It was evident that some go-to-market strategies became outdated and lost their effectiveness, mainly because of the mass adoption of similar strategies, new technologies, and software engineering budget savviness. And yet, what was agreed upon inside the room was not widely known outside of it. We saw, and we are still seeing investors backing companies and founders who build businesses and operate in ways that do not address the reality of the market.

This led us to perform 70 in-depth interviews with successful software infrastructure founders, engineering executives, and industry experts, to collect data and extract industry-relevant insights. Today, we reach a major milestone in this journey, which we have titled ‘Shift Happens’, and unveil our learnings on the evolution of Software Developer Life Cycle.

To portray the growth of the Israeli SDLC startup ecosystem, this report is divided into two parts: First, we showcase the great opportunity that emerged in Israel and introduce Grove Ventures’ Israeli SDLC Startup Landscape. In the second part, we unveil key findings about software engineering organizations and share best-in-class insights about how to build an SDLC-focused startup.

Part I – A Shift in the Market: The Israeli SDLC Startup Landscape

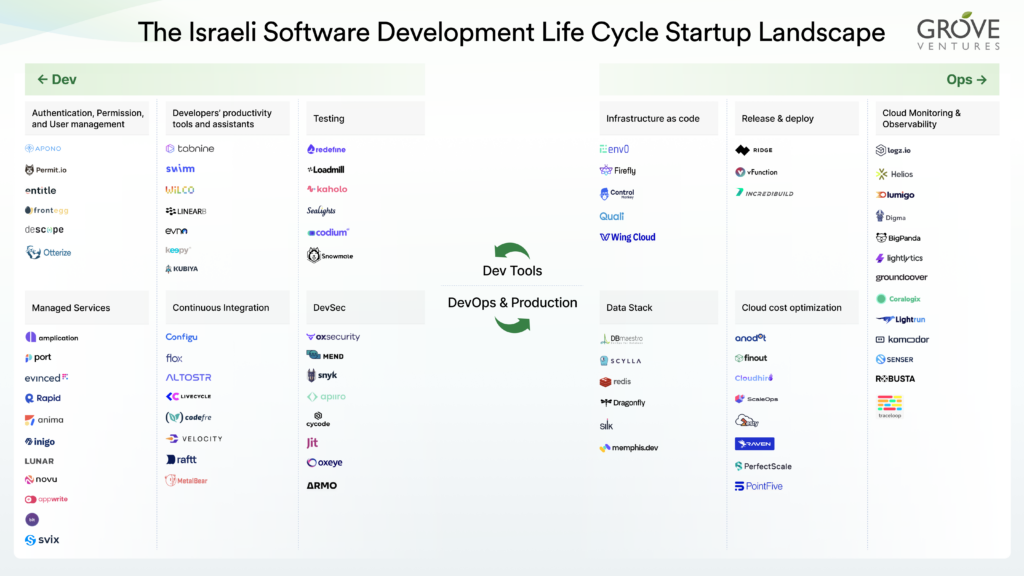

Israel is world-renowned for its cutting-edge technology. Although the country is widely recognized as a Mecca for Chief Information Security Officers, an equally interesting story is not getting the attention it deserves: Israel as a powerhouse of solutions for software engineers. With 100+ SDLC-focused startups and more than $5B in capital raised in less than a decade – almost a third of which in the past three years alone – Israel is the country of origin of category-leaders like JFrog, Redis, Snyk, and others.

To shed light on the Israeli SDLC industry, we mapped the eighty most prominent Israeli startups in the field, excluding public/exited companies, and in accordance with end-users point of view, following the software development life cycle, from left to right:

Download Map

The continued momentum of Israeli SDLC-focused startups, we believe, has two unique characteristics that contribute to its strength and potential:

The country became a massive buyer of developer-oriented solutions, products, and services – in billions of dollars a year. Traditionally, Israeli startups suffered from being distant from their target markets, which hurt their chances of achieving product-market fit. After a strong decade, things have changed. Dozens of Israeli companies were created with many gaining global scale, and the country became home to large engineering organizations. It became easier for founders of SDLC-focused startups to find partners that can provide important feedback early and within reach. In addition, Israeli companies themselves were now huge customers, which signaled to other enterprises around the world that Israel is a place worth doing business with when it comes to SDLC-related innovation.

A significant number of companies are led by second-time entrepreneurs with past experience in the buyer’s side of SDLC-focused products. This new generation of software-infrastructure-focused founders comes with profound domain expertise and years of market engagement.

Part II – Shifts in How People Buy, Use, and Plan their Go-to-Market: The Israeli SDLC Ecosystem Survey

To cut through the noise, we decided to dive into the data and conduct thorough research about the sector.

Our Methodology

We interviewed dozens of prominent industry leaders and gathered top insights from (A) Israeli founders of successful early-growth-to-IPO SDLC-focused startups, and (B) their customers (CTOs, VPs of Engineering, VPs of Platform and Heads of DevOps and Infrastructure), from both Iocal and global growth stage companies and public enterprises.

We intentionally started with customers: engineering executives who lead development teams and oversee software infrastructure budgets.

Our aim was to bring valuable insights to the surface, shed light on new market paradigms, and better understand the processes involved in the development, marketing, and adoption of products for the software development life cycle.

Where is the Money?

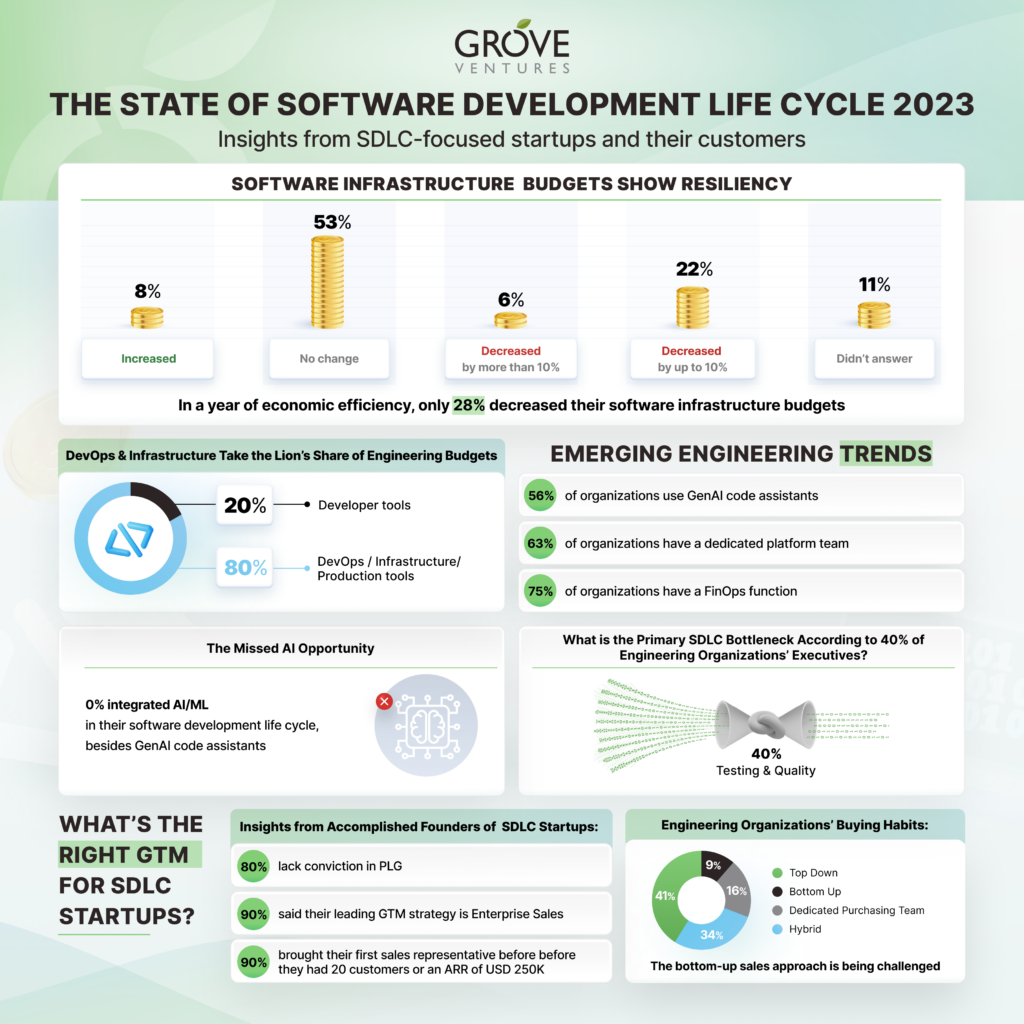

Even in a year of economic efficiency, software infrastructure budgets remained resilient. In a year of economic efficiency, only 28% decreased their software infrastructure budgets.

When asked to describe their budget allocation, engineering executives estimated that they spend equally (50/50) on Developer Tools and DevOps/Infrastructure/Production products. However, in reality, when we went over with customers on their major vendors list and calculated their actual expenses as part of our research work, a surprising figure was discovered: 80% of the engineering budget is devoted to DevOps/Infrastructure/Production tools, while only 20% is dedicated to Developer Tools. One explanation to these budget allocations may be that budget owners do not always separate their engineering spends by departments, and founders of companies that provide Developer Tools therefore receive a small portion of engineering budgets. This underscores the significant value customers place on DevOps/Production tools. While DevOps return on investment is clear, some customers explained, finding business justifications for Dev Tools is very difficult.

Emerging Trends

Israeli software engineering organizations have an early-adopter mentality and sometimes adopt trends even before they become mainstream. Here are some of the key trends and practices we identified in our industry survey:

Trend #1: GenAI Opens a Window for Mass AI Adoption in the Software Development Life Cycle: AI is certainly a prominent buzzword this year with Github’s Copilot activated by more than one million developers in over 20,000 organizations. We wanted to understand how this AI revolution has affected the software development life cycle. Here’s what we discovered: the majority of organizations (56%) have already started to implement GenAI code assistants. Other than that, however, no one (0%) integrated AI/ML in their software development life cycle. Although software engineers are usually at the forefront of technology, we discovered they are cautious about implementing AI solutions, with the main reasons for their unwillingness being regulation, skepticism, and trust issues.

Trend #2: Platform Engineering is on the Rise: Earlier this year, platform engineering was selected by Gartner as a Top Strategic Technology Trend. Our research discovered that this assumption has a hold in reality: 63% of surveyed organizations have a dedicated platform team in 2023. Although the adoption percentage is high, it was repeatedly mentioned by engineering executives that platform engineering should be treated like a design partnership that never ends: it addresses challenges of entities with ever-changing needs, and therefore dedicated engineering platform teams should constantly update their products. Each company has its unique approach to the discipline of building and operating internal developer platforms for software delivery and life cycle management.

Trend #3: Testing and Quality are Still the Main Bottlenecks: 40% of surveyed engineering executives mentioned ‘testing and quality’ as their primary software development bottleneck. And yet, executives did not “put their money where their mouth is”: Only 20% built in-house platforms for testing, and only 4% spent more than $25,000 annually on testing tools. Testing and quality is one of the hottest GenAI business verticals, and therefore we believe that this gap is likely to narrow.

Trend #4: Organizations Put an Emphasis on Being Cost-Aware – and FinOps Adoption Skyrockets: While software infrastructure budgets demonstrated resiliency, our survey shows that in 2023, 75% of respondents already have a FinOps function in their organizations. In 2022, FinOps Foundation estimated that 41% of organizations adopted a FinOps function. This significant growth in FinOps adoption was driven either by a real engineering culture shift or by the fact that 2023 was an uncertain year which resulted in an unusual desire to save on development costs.

Unlocking Go-to-Market

Many topics come and go, but the right go-to-market strategy for SDLC startups always sparks a conversation, with some founders who strongly believe that sorcery is required to decipher it. We thought it is high time to reveal what’s recommended in the market, and here is what we discovered:

Founders Lost Faith in the Product-Led Growth (PLG) Model: We believe that in order to find new opportunities, we have to challenge our assumptions to discover something new. We asked founders to share their contrarian view on the market, a truth that they know and no one else agrees with. A staggering 80% of founders offered the same ‘atypical market perspective’ when asked: they lost faith in PLG. The term PLG was coined in 2016 by OpenView, and is defined as a growth strategy where the product itself acts as the primary driver of acquisition, retention, and expansion. It immediately became the main go-to-market model for most software infrastructure companies. As this strategy became more and more popular, the competition for the individual developer’s attention surged and standing out became harder than ever. The widespread adoption diminished the competitive advantage previously associated with its implementation.

Founders Agree: Enterprise Sales is the Preferred GTM Strategy: When asked about which go-to-market strategy actually works, 90% of founders mentioned enterprise sales. The majority of growth-stage companies actually prefer a mixed method: they rely mainly on outbound enterprise sales and use PLG as a marketing method to increase brand awareness and build inbound demand generation.

Sales Representatives Join Early, Working Alongside CEOs: Many founders debate what is the right time to bring a professional salesperson on board. Usually, founders are advised to reach product-market-fit by selling their product hands-on and delay the hire of a professional sales representative. Surprisingly, 90% of founders in successfully scaled SDLC-focused companies brought their first sales representative before they had 20 customers or an ARR of USD 250K. Mostly, founders kept a ‘hands-on’ approach with their customers, and used the sales representatives to help with lead generation and sales operations. In retrospect, many founders said they would have brought in a sales representative even sooner.

Organizations Assure: Bottom-Up Sales are at the Bottom: Over the past decade, the ruling assumption was that engineers could pick and choose their own development tools, and startups heavily relied on PLG and bottom-up sales. However, it turns out that founders should not be ‘religious’ about creating bottom-up motions. Our research suggests that only 16% of companies purchase dev tools bottom-up. 41% adopt products top-down, 34% use a hybrid purchase method, and 9% have a dedicated team of ‘gatekeepers’ that decide on the purchasing of any new software development life cycle product. This marks an additional paradigm shift and corresponds with the founders’ lack of faith in bottom-up PLG.

In the ever-evolving Israeli SDLC landscape – a shift has happened. Innovation pushes the industry forward, and founders, once spellbound by Product-Led Growth (PLG) strategies, now understand that enterprise sales are key to the success of their businesses and must be championed. GenAI, Platform Engineering, testing, and cost-efficiency considerations echo through the industry. As the ecosystem grows and develops, it is important to be able to adapt, respond, and let the learnings and wisdom of successful companies and individuals light the path.

Download Presentation

Send Us Your Feedback and Join Grove Ventures’ Shift Happens Community

The software developer life cycle continues to evolve. At Grove Ventures, we started an ecosystem discussion about the first market insights we gathered as part of this survey back in May, at our first ‘Shift Happens’ event – Israel’s summit for top engineering executives and founders who shape the future of the software development life cycle. We were joined by more than 130 prominent leaders in the sector as well as leading global companies from all over the world. We invite you to challenge our perspectives and share additional thoughts and insights:

To join our Shift Happens community, please fill in this form.

Special thanks to Daniel Ben Zvi, Uri Schiner, Ofir Ehrlich, Aner Mazur, Zack Smocha, Amit Attias, Ofer Kirshenbaum for reading drafts and contributing their thoughts.